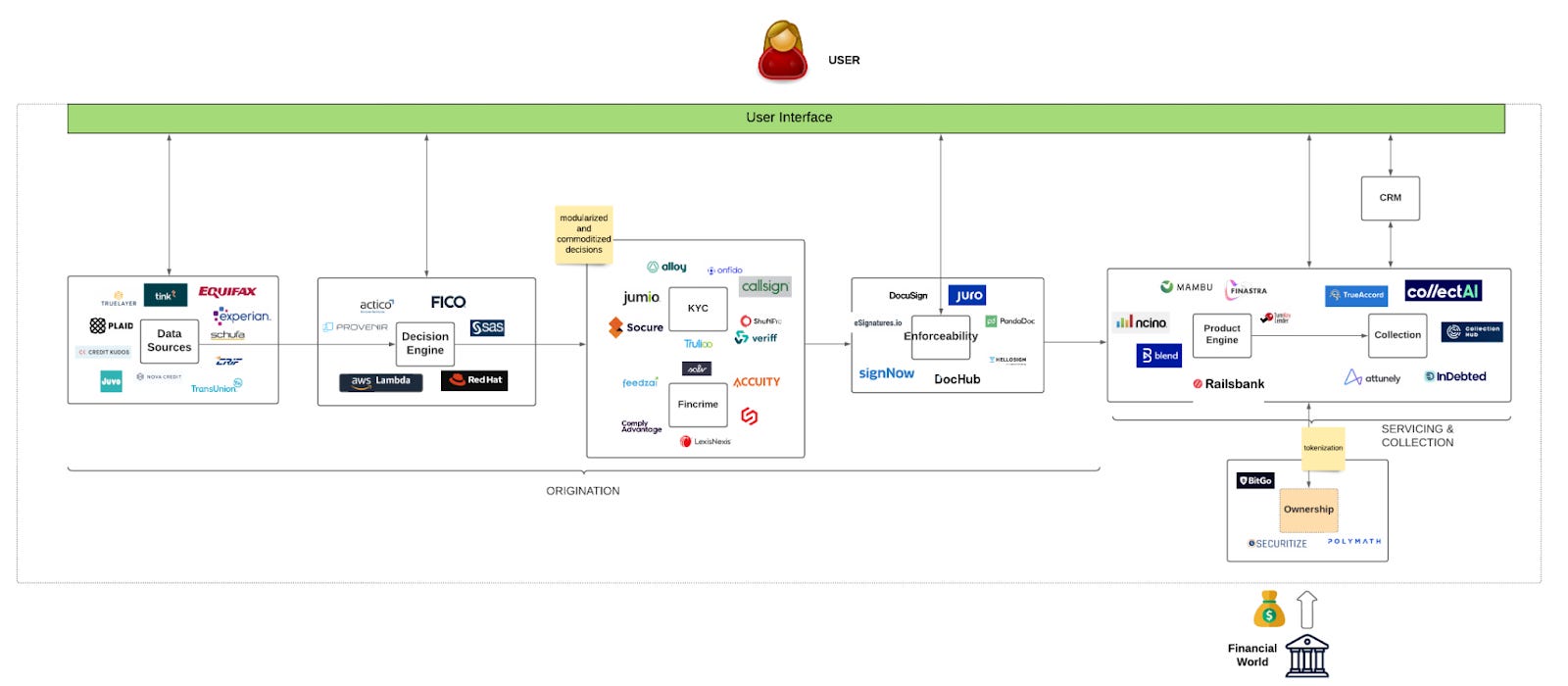

Last fall I wrote a post that described the key component of a retail banking business. The following post is the ideal complement to ‘A neobank stack’ and the goal is to describe the key elements of a lending stack, adding some new DeFi pieces to the architecture.

Overview

In my experiences at Funding Circle and N26, I spent a lot of time working on lending products and my main takeaway was that lending money is a business built on two critical ingredients: mathematical models and data.

What underwriters do is to take a set of data points, related to the loan applicant, and plug them in a mathematical model (from now on risk model). This model will produce a number which is a proxy of the creditworthiness of the applicant.

Based on this proxy they will then decide if they want to extend an offer to the borrower and at which price, i.e. the interest rate.

The precision of the credit decision is thus a critical factor for the success of the lender: if the lender can’t correctly predict the creditworthiness of the borrower, the result could be catastrophic.

These decisions were once made by the people working in banks, following some semi-standardized decision frameworks (the most common for retail lending were called CAMPARI and ICE). As technology progressed, lenders started to use a more efficient machine, computers, but the nature of the problem they were solving didn’t really change: ultimately, a credit stack is nothing else than a glorified decision-making computer that makes decisions at scale on an array of dimensions.

Data Sources

Being lending a business of data and math, having the right data sources is essential. In the past, lenders relied mainly on application data (manually input by applicants) and credit bureaus. With the advent of smartphones, social media and open banking, many more data sources are now available.

Data sources are usually geo-specific so every country will have its own credit bureaus that lenders have to integrate to. This brings a lot of complexity to scaling your product across multiple countries, because you will have to integrate new data providers and re-train your risk models (the formulas that generate the proxy of the borrower’s creditworthiness) on the new data sets.

In addition to this, it’s important to note that nowadays it is very hard to build a competitive advantage on data, as most of the sources available are non proprietary - any lender could buy access to that information and use them.

Decision Engine

This is the system where risk models are developed and used. It is generally a third party software for decision making that lenders connect to the data sources seen above, and where more or less complex risk models are deployed.

A good decision engine usually provides an integrated training environment that allows the lender to constantly re-train the risk models, which means to re-optimize the ‘formula’ based on new data points and on the feedback coming from the active loans. These updated versions of the model should then be easily - and, ideally, automatically - promoted to the production environment.

Decision engines are very important because they work in the same domain space as risk models, which are considered one of the most important competitive advantages in lending. I strongly suggest this post by my former colleague and friend Rohit to get a deeper exposure to underwriting.

KYC and FinCrime

Credit decisions are not the only decisions that a lender will have to make throughout the loan application. Other dimensions that will require a decision are: Fraud, AML, KYC.

The lender will have to check if the applicant is who they claim to be, if they have any fraudulent activity in the past, if there is a suspect money laundering activity, plus extra checks on political exposure.

These decisions are fairly standardized and commoditized and it makes a lot of sense to use providers to delegate them.

All these elements don’t constitute a primary competitive advantage but they are extremely critical given the regulated nature of the lending business.

Enforceability

Once the lender has made a decision on the borrower, they must make sure that the loan contract will be legally enforceable. Concretely this means that the contract will have to be signed and the ownership of the asset, eventually used as a collateral, will have to be verified.

There are many service providers that give access to easily integrate digital signature solutions.

The validation of the collateral ownership is instead still mostly a non-automated service and that piece of the process is not really part of any stack at the moment.

My expectation is that this element will be fundamentally transformed by blockchain technologies: most of the objects that we can use as a collateral are very easily representable as NFTs. If a user’s car could be associated to a NFT on-chain, they could instantly get a loan from a lending service online simply using the ‘car NFT’ as a collateral that the lender could very easily track and lock - on-chain.

Loan Servicing: Product Engine & Collection

The loan servicing phase of a loan starts after a loan is closed and originated: the lender made an offer to the borrower, they accepted it and now it is time to manage the recurrent flow of repayments and apply it to the loan balance, and eventually missed repayments.

The servicing phase includes two core functional pieces: the product engine and the collection service.

The product engine is a software that allows the lender to build different credit products at scale. This software allows you to configure a new product by just setting some critical variables like type of product, interest rate structure, repayments frequency, early/late repayment options, etc…

Through these services, lenders can now deploy new credit products in minutes, a speed order of magnitudes faster than with the previous technological paradigm.

The collection service is the process to deal with late or defaulted loans and it substitutes in-sourced collection teams or inefficient - and hard to track - collection agencies.

Given its recurrent nature, this phase is closely linked to the user and it represents a strong opportunity to build a competitive edge: as data sources are getting more and more standardized and risk models are a hard to build USP, a flexible servicing experience can represent a low hanging fruit to leverage.

Ownership

The original lifecycle of a loan was once pretty straightforward: the bank assessed the creditworthiness of a loan applicant, made an offer, if the offer was accepted the bank disbursed the loan, and then it would collect every month the expected dues.

With the evolution of the financial industry, due to regulatory and risk reasons, some other lifecycles came into existence, the main one is called originate to distribute: banks still “originate” the loan (assess the creditworthiness of a loan applicant and disburse the loan) but then, it doesn’t wait anymore for the collection of the loan repayments. Banks instead “distribute”, which means sell, the loan to some other investor, who actually owns the claim rights on the repayment flows. The bank will not get the repayments, the investor will.

This form of loan lifecycle is now probably the most frequent in circulation but, to make it happen, a complex organizational unit - including an army of lawyers and a sizable tech team - is needed.

Today there is no well adopted service that allows the programmatic transfer of the ownership of financial assets in a modularized and standardized way.

Yet again, in my opinion, this is where blockchain-based services will eventually step in: every loan will essentially be turned into a unique digital token (NFT) and then it could be traded and distributed at a speed and cost that is 10-50x better than today’s.

Conclusions

In this post I wanted to give an overview of what a consumer lending stack could look like, starting from atomized problem spaces.

As you probably noticed, I introduced a certain number of blockchain references to the picture: my expectation is that lending will be the first industry where cross pollination between TradFi (traditional finance) and DeFi (decentralized finance) will happen, especially around asset tokenization.

Over the next months, just for fun, I will build a prototype of this end-to-end stack from origination to tokenization. If this sounds exciting to you and you have fresher tech skills than mine (ideally Python scripting, API integration and some experience with Solidity), please ping me.

Resources

CAMPARI AND ICE frameworks - LINK

SMB Credit Decisioning framework - LINK

Credit decision stack by Sandi Samantaray - LINK

Lending Competitive advantage by Rohit Sharma - LINK

Embedded finance opportunities by Rohit Sharma - LINK

Framework for a credit startup by Rohit Mittal - LINK

A brief guid to starting and building a lending business by Rohit Mittal - LINK

Securitise and Tinlake partnership - LINK

JPMorgan's CEO Jamie Dimon letter to shareholders 2020 - LINK