A neobank stack

Over the last few years I’ve spent a lot of time building lending and banking stacks. What used to require vast resources only 10 years ago, is today a much simpler and more inexpensive job, thanks to the enormous number of financial infrastructure businesses born in the last decade.

The goals of the following 2 posts are: to highlight which are the key functional components of these stacks, to point at who are the main providers around and, more in general, to share what are some of the key learnings I gathered working hands-on on their development.

An overview

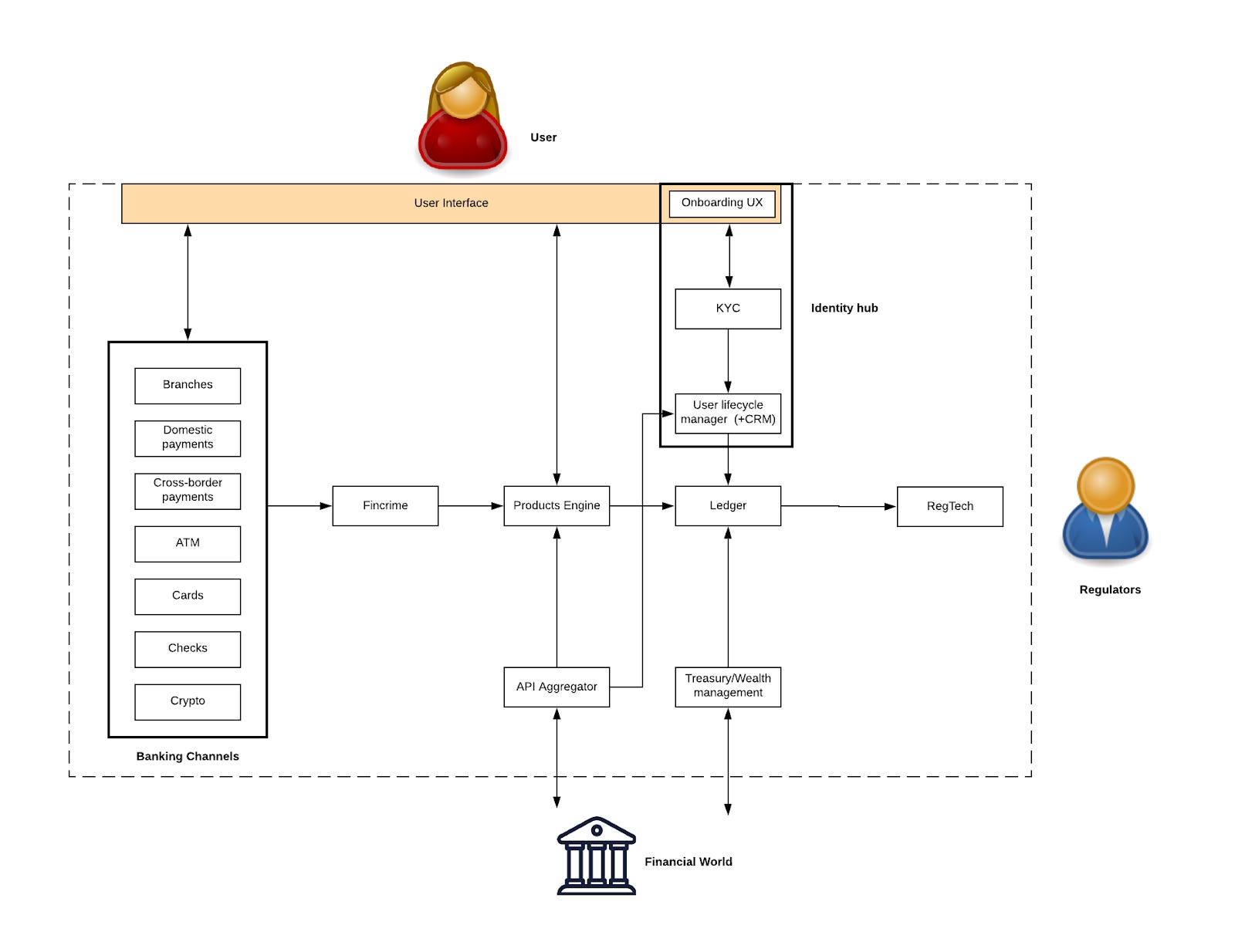

The core assumption behind this architecture is that a retail bank is not in the business of making mobile apps, nor it is in the business of issuing debit/credit cards. A bank operates in 2 problem spaces:

the business of trust (liability side) - a bank is an institution selling trusted repositories where users can store their value. It must convince people that it is a trustworthy institution.

the business of selling liquidity (asset side) - a bank must make a profit out of the funds it gathered, correctly setting the price of the liquidity, based on the risk profile of its clients - on the asset side

The average banking product is simply an interface optimised for the current state of the technology: today it is a smartphone application, in the past it was a branch, in the future it will likely be a different interface. What won’t change are the fundamental problems that a bank will solve, as shown in the architecture designed below.

Banking channels

This module includes multiple elements: from domestic payments to branches, from ATMs to cryptos. These apparently very different pieces have one core characteristic in common: they enable the movement of money inside and outside of the user account. Each one is a different touchpoint which covers different use cases for different demographics, but they all ultimately enable money movement.

I believe this module is probably the most affected by the modern banking evolution, putting together today things that were completely different in the past, such as Cards and Branches. Take branches, for example. As the retail banking space evolved, the branch-centric approach has been totally surpassed and branches pushed to the margins of the banking architecture.

Branches today are to banks what CDs are to songs: once the physical embodiment of the service, now they are nothing more than a nice accessory, interesting to some, but definitely not a central component of the related business model.

In the banking channel alone, there are literally hundreds of companies trying to build more modern API-based experiences which requires minimal effort to integrate with and guarantees adequate support.

Fincrime

The Fincrime module is in charge of filtering out potential fraudsters and money-launderers from the flow of total movements. It is logically a clear extension of the banking channels component, because it operates on top of those transactions.

It is a fairly recent innovation which became necessary when banking lost its personal touch and became a machine-first, more than a person-first, business.

Fincrime is one of the spaces where artificial intelligence and machine learning techniques are seriously delivering value: it would be inconceivable for a modern bank to manually or semi-manually scan all the transactions.

Products engine

The product engine is probably the flagship element of modern core banking platforms. It is a product configurator where a bank can easily configure standardized products like overdraft, checking account or loans and immediately distribute them to its customer base.

It is usually bundled together with other modules in a wider core banking offering (ledger).

NB. In my abstraction, the product engine does contain the creation of the loan, credit line and overdraft products, but doesn’t include the decision lending stack, which I’ll present in a future post.

Ledger

Ledger technologies have been the foundation of any banking businesses since the northern Italian city states invented banking just after the Middle Ages. A ledger is nothing more than a glorified database, and it represents the ultimate source of truth on the account balance and, in general, on any banking activity within the company.

A ledger must be extremely reliable, secure, easy to integrate with and easy to query.

Being blockchain a ledgering technology, this domain is constantly mentioned as being a domain ripe for innovation. My opinion is that blockchains, before being ledgers, are primarily systems to align incentives and I’m very skeptical about the real benefits of permissioned chains. For this reason I believe that DLT doesn’t really make sense today as a ledgering technology for a bank, especially in a permissioned context and without a proper ecosystem built around it.

API Aggregator

API aggregators are new-comers to banking. Before open banking took off, this element wasn’t even a theoretical concept in banking ecosystem.

Today, almost every bank is integrated to at least one banking information aggregator which shares data about customers gathered from other financial institutions.

The role of API aggregators is still in its infancy but, being banking a business of information, I believe that their role will become more prominent over the next years.

Identity hub

I decided to aggregate Onboarding, KYC and CRM because they represent to me different phases of the same user’s lifecycle, as they all build different aspects of the identity of the user in the bank's eyes.

As user onboarding moved from a branch-based approach to remote, KYC providers acquired an enormous space and there are a lot of companies doing KYC cheaply and very reliably in the vast majority of geographies.

Identity is surely a banks’ key asset but its value still remains largely untapped, as no bank built a business on top of the constellation of information gathered on the users, nor on facilitating dedicated identity services to other providers.

Treasury

Putting the capital gathered in its deposits to a more productive use is one of the key activities of a bank. This is a crucial activity for bank profitability, but this also requires skills completely different from the ones typically available in a consumer-focused neobank. All the recently funded neobanks tend to be very user-centric and customer-service focused: they are 21st century technology companies more than traditional financial companies, therefore scaling up this function can be extremely defocusing in the growth phase, when the goal of the bank is to create a solid customer base of depositors.

In this scenario, many of these companies can outsource their treasury investing/activities to some of the many investment vehicles around or can, more traditionally, use softwares to internally manage their liability side.

RegTech

The financial industry is one of the most regulated industries in every country and a tremendous amount of resources is spent on this activity. Lots of companies are working in this space.

Conclusions

In this brief post I wanted to present some high level modules that I believe are essential elements in building a modern bank.

All the brands and companies mentioned are only a small subset of the incredible number of good solutions in circulation and most of them cover more than one aspect, but this is not factored in in my architecture.

In my next post you will find a similar exercise for the other crucial stack of a bank: the credit decision stack. Stay tuned.