Adyen, payments made easy

As my fellow Product Peon taught me a long time ago, the best way to learn quickly how a specific company works, is to analyze its 10k. For this reason, in the Fintech Product Guild, we decided to start a '10k-a-month' club. This month we analyzed Adyen, a payment company.

What does Adyen do?

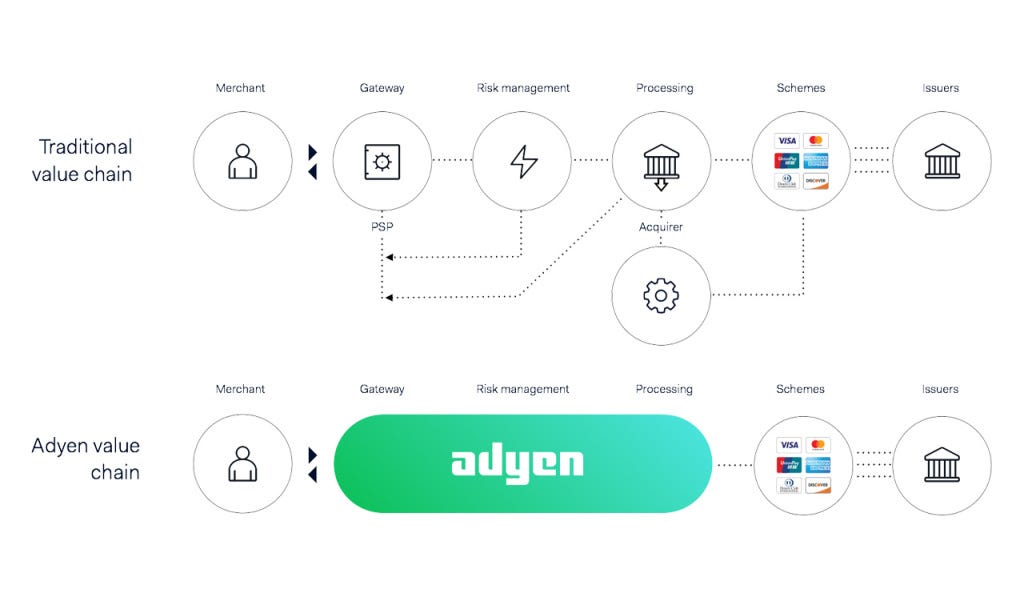

Adyen was founded around 15 years ago to facilitate the adoption for merchants of electronic payments. At that time, the payment chain was extremely fragmented with multiple players coordinating different pieces of the chain: gateway, processing, risk management, acquiring (more on the evolution of the payment industry here). Adyen approached the problem from a different perspective: they built a merchant centric product, a payment-as-a-service infrastructure which essentially made the process of accepting a payment much easier for their merchants.

The venture went very well, they secured a lot of fundings and went public in 2018. Today Adyen is a public company which offers a payment platform to support the growth of its merchant through various ways:

a wide range of payment methods accepted

quick plug and play scalability in new countries

user-centric checkout solutions to improve merchant conversion rates

fraud prevention

Financials analysis

Income statement

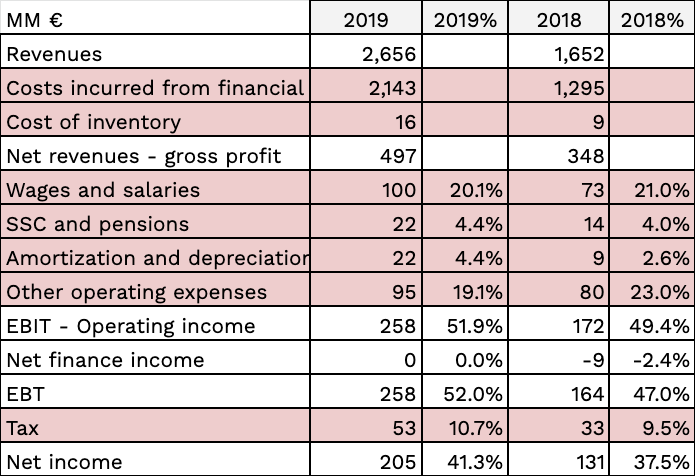

Over the last 3 years Adyen saw a sustained growth, with its total payment volume growing 1.5x from from 2017 to 2019 that directly transacted into a 2.5x growth of the net revenues.

Their revenue model is based on four elements:

Settlement fee: % of the value for acquiring services (to be netted of interchange fees)

Processing fee: fixed fees (10 € cents) paid when a transaction is initiated via the Adyen payment platform

Sales of POS (Point of Sales)

Other services: exchange service fees, 3rd party commision

From a gross revenue perspective, the settlement pillar appears as the dominant component of their business, with a contribution of more than 85% to the total revenues.

Anyhoo, the situation looks different when we consider the net revenues component.

In reality, considering their holistic approach to payments, it is obvious how each component of their product self reinforce the others: they offer a single package which aims at solving every problem of the payment cycle and each business line should be analysed with these lenses - losing a few millions on the POS business is a no brainer, when this will lock in the merchant and guarantee extra Billions of € of transactions on the platform.

Overall, they show a pretty solid growth of revenues and a very strong operating margin (over net revenues), which sits around 51%. This is a very healthy margin, especially when compared to other competitors in the space.

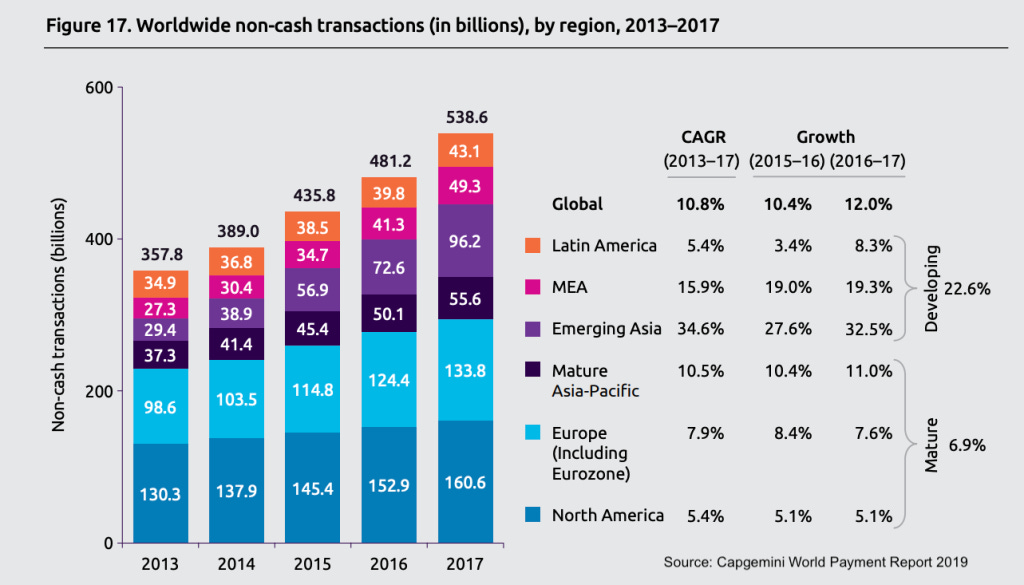

Adyen's growth over the last years has been impressive, but this must be contextualized in a favorable trend for the entire payment industry. The revenues of the global industry more than doubled in the last decade and the expectation, based on McKinsey Global Payment Report, is that they will grow even further in the next 3 years.

In this already positive wider environment, Adyen benefitted even more from the shift away from cash towards electronic payments - with a total number of non-cash transactions almost doubling in the last 5 years.

Balance sheet

The biggest insight deducible from the BS is that, not surprisingly, payments is such a liquid business! 67% of Adyen assets are in cash or cash equivalents, and 19% are Receivables for a total 86% of current assets.

Looking at the common size analysis, the sheet shows a strong continuity with the previous year. Most of the items didn’t significantly change from 2018, with a clear organic expansion of the BS.

Statement of Cash Flows

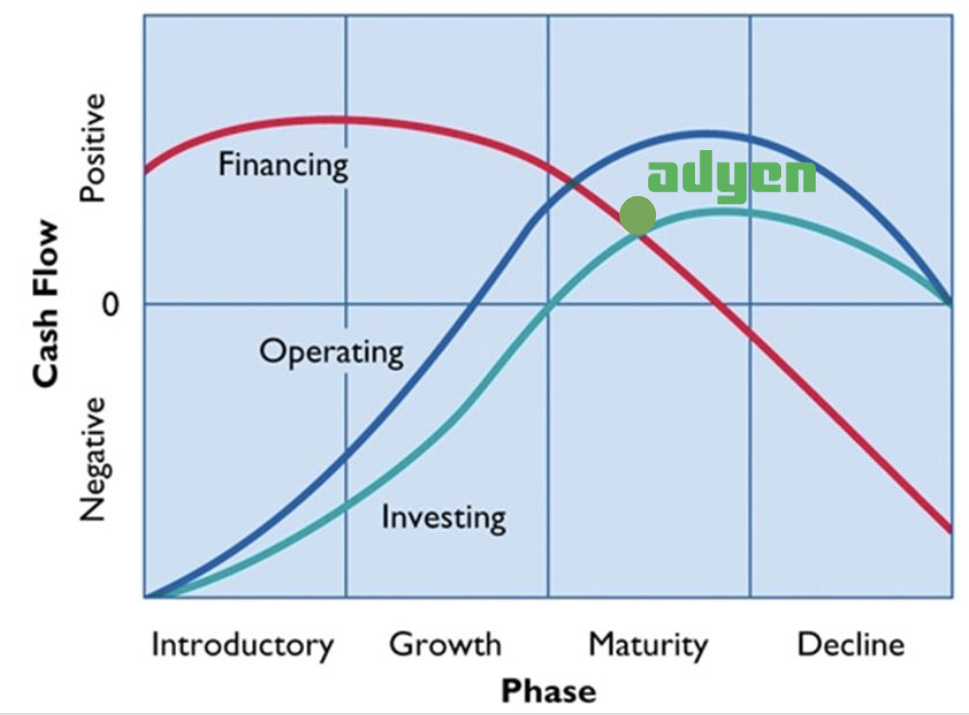

The SCF is in line with the growth story told by the Income Statement and Balance Sheet. Adyen presents a positive operating cash flow which grew steadily in parallel with the net profit, with minimal net financing and investing flows.

If we abstract that trend and represent it in the typical cash flow curve, we identify a company in its late growth/maturity phase: a company which is producing strong operating cash flow, it's not highly negative on investing anymore but it is also not distributing back to investors yet.

Looking ahead

Adyen's financials describe a company in great shape and ready to scale its business further very quickly. Even though it is playing in a crowded industry, the Dutch company is in perfect position to become the go-to payment platform in particular for enterprise customers who want a modern, digital-first payment infrastructure - less so for SMEs who would probably look at more self-serve platforms like Stripe.

The recent pandemic will probably only accelerate their growth, due to the obvious shift to digital products of many users, a segment where Adyen is much better positioned than many incumbents in the space.

Overall, Adyen is definitely a solid company with a very scalable business model and a promising future.

Resources

Adyen:

https://www.adyen.com/investor-relations/publication-annual-report-2019

https://medium.com/iveyfintechclub/how-adyen-is-disrupting-payment-processing-7e0e261f0ea

Payment industry maps:

Pricing: