Visa 10K: the mother of all protocols

The last session of the 10K-a-month club was focused on one of the most interesting companies in the financial ecosystem: Visa.

Visa is probably one of the most ubiquitous brands on the planet: you can recognize its logo on virtually every shop, from boutiques on the Champs-Élysées to a mini-store in Mongolia or the checkout page of an Australian florist.

In its essence, Visa is not a financial company: it is an information company that runs a centralized payment protocol and makes a huge volume of transactions possible. Visa does a simple but incredibly powerful job, as it enables card payments for users, allowing banks to talk to each other and clear payments. Its role in card payments is very similar to the role that SWIFT has in correspondent banking, which I described in a previous post a few months ago.

HISTORY

There are various books and posts around that describe the history of Visa and I strongly recommend Joe Nocera’s ‘A piece of the action’ and ‘Electronic Value Exchange’ by David Stearns.

Visa started its operations in the summer of 1958 when Joe Wilkins, an employee of Bank of America, proposed to create a payment card system similar to the Diners program, and called it BankAmericard. 60k units of BankAmericard were shipped to the city of Fresno (The Fresno Drop), where Bank of America had a penetration of approximately 45% of the population.

The product allowed users to pay with this card that had a credit line connected to it. As every MVP many things didn’t work: lots of fraud and default happened, over 22% of the repayments came late, but Visa didn’t give up and, by the mid-60s, the product was generating profits.

Then the hardest phase started: expansion. BankAmericard created a licensing program, guaranteeing to them a setup fee plus 0.5% of the total spend, in exchange for transferring the know-how of running a credit card network to any licensed bank. Various banks joined the program, people used this card, but the ecosystem was highly fragmented.

Thanks to the work of some industry pioneers (first of all Dee Hock – the legendary CEO of VISA), the renamed National BankAmericard Inc. became the connector among the banks who were part of the licensing scheme, and unified this fragmented ecosystem into a single consortium of banks.

In the end, two consortiums emerged: National BankAmericard Inc. (then renamed Visa) and MasterChange (then renamed MasterCard).

Over the last 30-40 years, Visa progressively consolidated its position in the payment space, becoming the strongest party to a de-facto duopoly. Yet, it was always considered nothing more than a glorified IT system by the banks which adopted the system. Definitely not one of the centerpieces of the financial ecosystem, as it is considered today.

In 2008, Visa went public, mainly due to antitrust and regulation reasons and launched one of the biggest IPO to date. Since then, as we will see in the next paragraph, the company grew at an incredible pace.

10K ANALYSIS

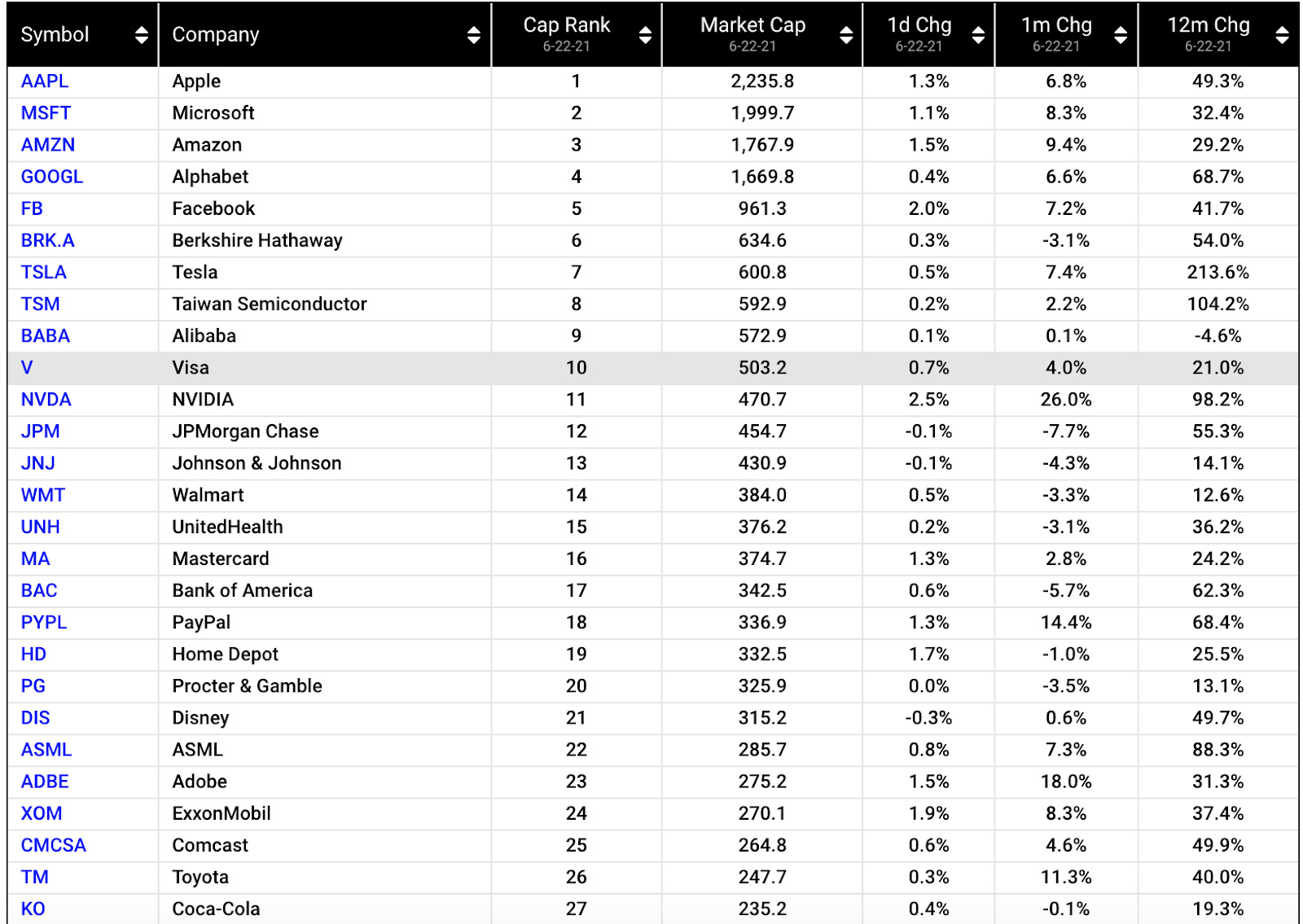

Differently from other 10Ks, I started this analysis by looking at the company’s market cap which, on the 22-06-2021, was over $500B and bigger than any bank in the Dow Jones – approximately 30% more than Bank of America, the entity that founded Visa.

During fiscal year 2020, Visa oversaw 204 billion payments and cash transactions, equating to an average of 559 million transactions a day, which means 390 thousands a minute and 6.500 a second. This volume is approximately 1000 times bigger than the number of transactions Bitcoin can process per second (7 tx/sec).

Out of the 204 billion total transactions, 141 billion were processed by Visa, while the others were processed by other networks on behalf of Visa (many of them were transactions on-us, so transactions where the issuer and the acquirer were the same institution).

At the end of June 2021, Visa’s total payments and cash volume stood at $11.3 trillion – of which $8.9T processed by Visa’s own network. 3.5 billion cards (BINs) were available worldwide to be used at nearly 70 million merchant locations.

All figures above are impressive and they present a company that is almost twice the size of its main alternative: MasterCard.

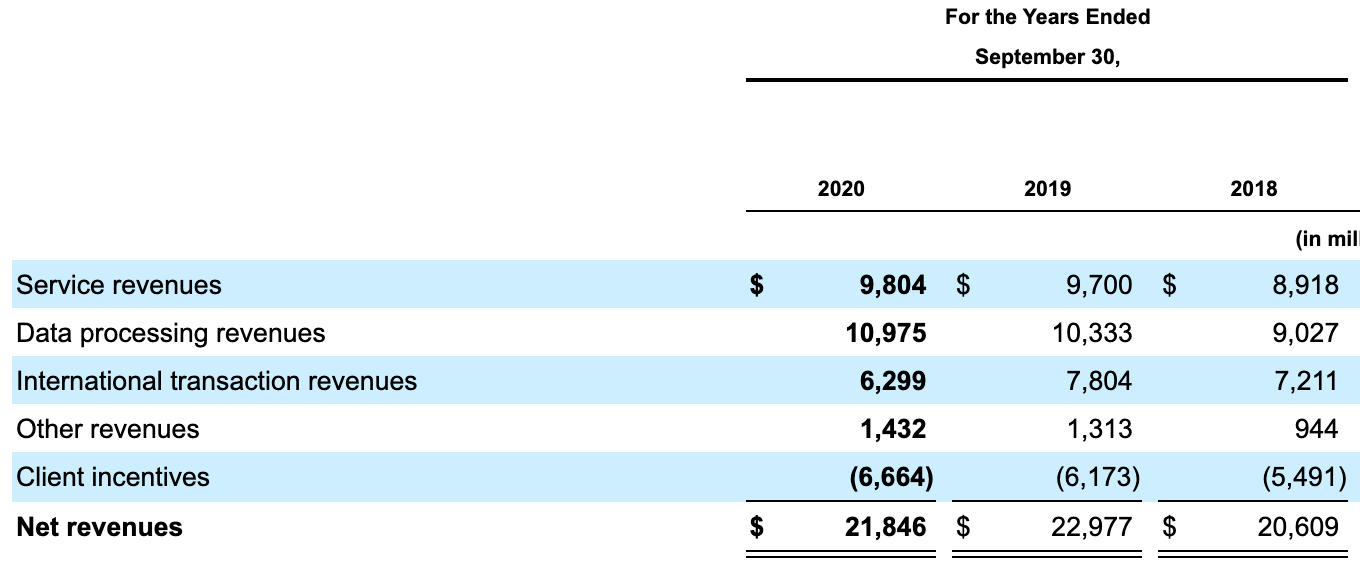

In terms of volumes, Visa generated over $28B gross revenues split among service ($9.8B), data processing ($11B), cross border transactions ($6.3B) and other revenues ($1.4B).

In 2020 the net revenues were slightly lower than 2019, at $21,8B and discounted a higher incentive stream than 2019, mainly directed at issuers.

Visa is subsidizing issuers so strongly (with over $6.5B in 2020), because issuers represent the real Visa customers.

Specifically, due to their role in the card payment transactions, issuers are those that ultimately control on which scheme the customers’ transactions will transit. An average Jane is pretty insensitive to the network of her payment card, so she doesn’t really care if it is MasterCard or Visa. It is the scheme itself that cares, because more cards translate into more transactions and thus more revenues.

So the scheme strongly incentivizes issuers to pick Visa, over MasterCard, as the issuing brand.

Another very interesting revenue stream is the international transactions’ stream: these are transactions made in a foreign currency (than the default one of the card) on which Visa has to perform some forex activities, which proves to be extremely profitable.

GROWTH OPPORTUNITIES

Visa mentions 3 main growth drivers in its 10K: cash conversion, new flows and VAS. Out of these 3, the first one looks to me the most solid one by far.

Yes, VISA can potentially tackle new use cases and support new flows but the competition there is very aggressive and I’m not sure Visa has the hunger and aggressiveness to chase new use cases – even though this is an estimated market of $185T according to Visa’s own 10K.

I believe that the real growth will come from the same source it did so far: being a strategic enabler of a secular trend of money digitalization. This is what made Visa more valuable than any other bank and this is what will allow Visa to grow even further.

There is approximately $18 T in consumer spending still done in cash and checks, which I believe will organically and progressively move to cards and digital credentials over the next decade, without any major product or distribution innovation, just as a consequence of the continued digitization of our world.

POTENTIAL THREATS

The question I wanted to answer in this paragraph is: “What has to happen in the world to make Visa less relevant 10 years from now?”.

A number of themes came up in the discussion with my fellow guilders. They were all extremely interesting – thanks in primis to Rupert and Philip.

Geopolitical threat. We are progressively moving from a unipolar world where one country was the only global superpower, to a multipolar world where various states compete to acquire this status. In a multipolar world, allowing one or two American companies to run such a critical infrastructure as digital payment systems, is a huge single-point-of-failure and a risk for other sovereign states. This could lead to the creation of new regional payment networks that could eventually hurt Visa’s penetration in that region. A fitting example is what happened in Russia where, after the 2015 sanctions, they successfully created and launched Mir, the Russian payment scheme, supported by the Central Bank of Russia.

Cross-border transactions. These are the transactions that the card user makes in a currency different from the standard currency of the card. They represent a very big chunk of Visa’s Net revenues but they are clearly built on the inefficiency of the system. Third parties involved in their processing and generation could find alternatives to run the same transactions at a fraction of the cost and hit a very profitable business segment for Visa.

Issuers/acquirers defection. If big issuers start acquiring more and more, or if big acquirers start issuing, they can autonomously close the payment loop and self-clear the transaction. Everybody that can both issue and acquire at scale (which means at least hundred of millions of BINs), will be in a very strong position, and they could seriously dent Visa’s position.

Big Tech. The wallet is moving to the phone. That is a reality which will only become more relevant over the next decade. This will put Google and Apple in a dominant position in the payment space, but I doubt they will battle any scheme. They will probably become another “tax” to be paid by issuers and acquirers, not very differently from Visa and MasterCard.

Fintech. I wrote a post some weeks ago in which I described Square’s attempt to build two complementary ecosystems that could in theory connect to cut Visa and MasterCard out. This hypothesis is highly fascinating and ambitious, and maybe in Jack Dorsey’s mind, but Square’s business still relies so heavily on card rails that it would be very unlikely that Square would challenge Visa so directly. The same can be said of Paypal.

Crypto. This is the most exotic theme, as crypto-currencies are the hottest topic in financial innovation. Ignoring the scalability aspect, which today is orders of magnitudes behind what needed to really hit Visa, crypto currencies proved to be anything but real currencies as people are not really spending them to buy stuff, which is ultimately the business Visa is involved in. I imagine some experiments and POC will continue in the space, with Visa using some chains, but I consider these initiatives more PR stunts than use cases precursors of the future. In general, I don’t think crypto will really impact the payment processing industry, as much as other pieces of the financial system.

CONCLUSION

Visa is clearly a fantastic business: a money machine that sits at the center of a critical infrastructure and the company is perfectly positioned to fully take advantage of a secular trend, the migration of payments from paper to digital.

That is what ultimately explains its huge growth in valuation over the last 15 years. Considering that this transition is far from over, my expectation is that the business will keep on thriving and prosper over the next several years.